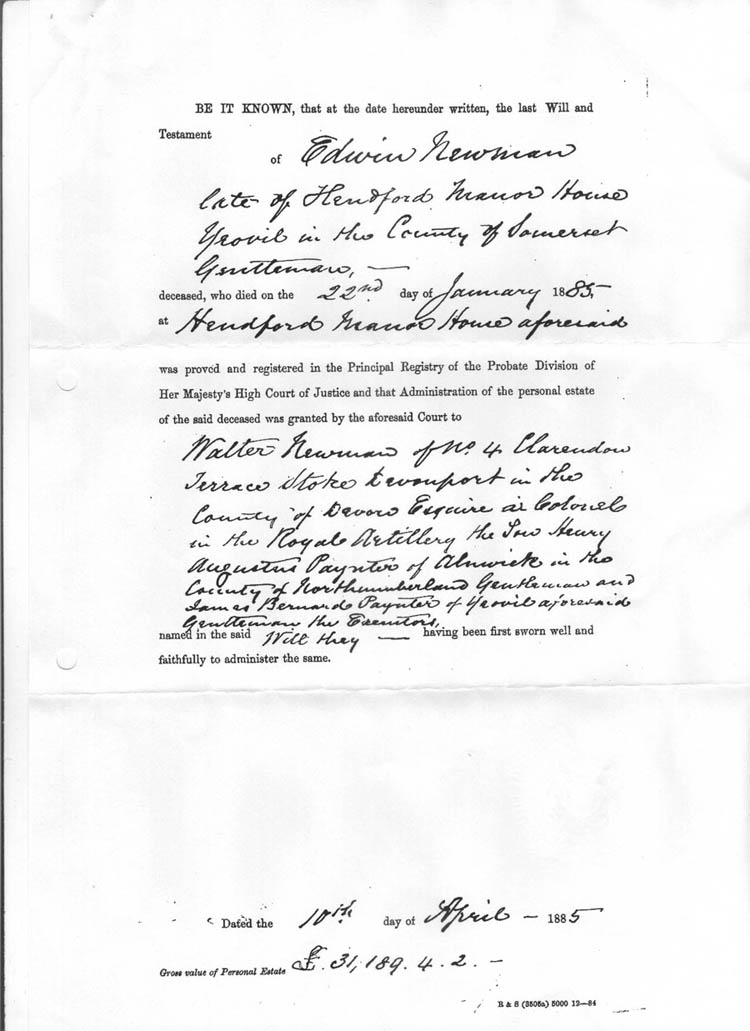

Edwin Newman's Will

Will dated 4th November 1884. Probate Granted 10th

April 1885

Note: A transcription of Edwin's Will can be found below including a breakdown summary.

Transcription of the Will of Edwin Newman –

died 22nd Jan 1885.

(Punctuation and paragraphs added by transcriber)

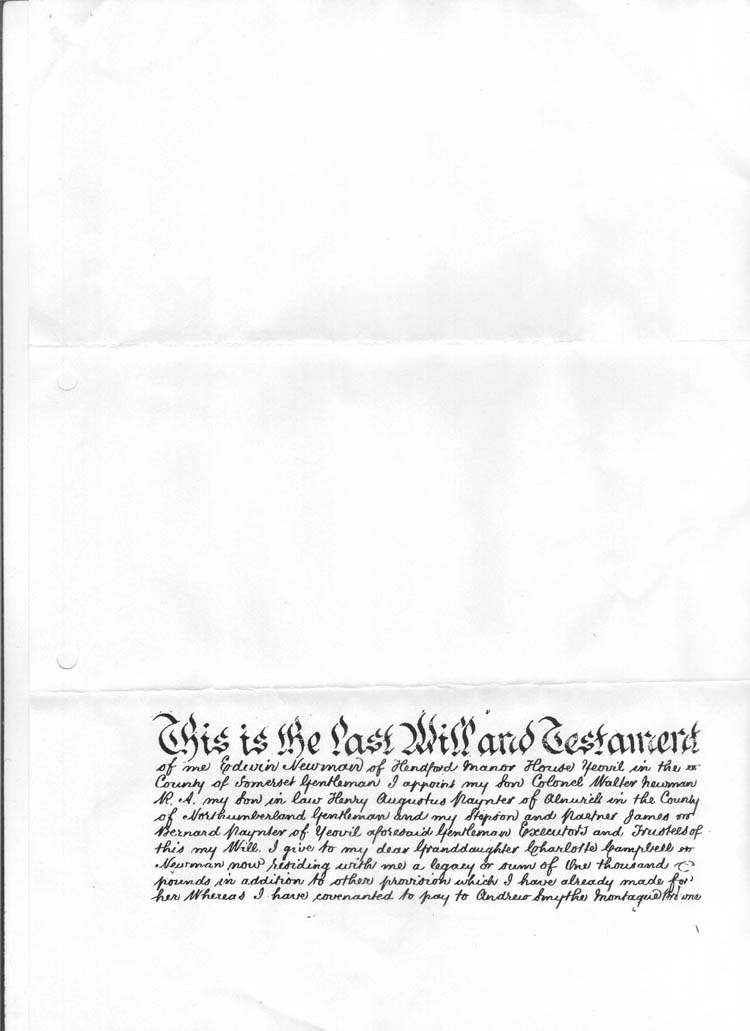

This is the last will and testament of me, Edwin Newman of Hendford Manor House, Yeovil, in the county of Somerset, Gentleman.

I appoint my son Colonel Walter Newman RA, my son-in-law Henry Augustus Paynter of Alnwick in the county of Northumberland Gentleman and my stepson and partner James Bernard Paynter of Yeovil aforesaid Gentleman Executors and Trustees of this my Will.

I give to my dear granddaughter Charlotte Campbell Newman [Lottie] now residing with me, a legacy or sum of one thousand pounds in addition to other provisions which I have already made for her.

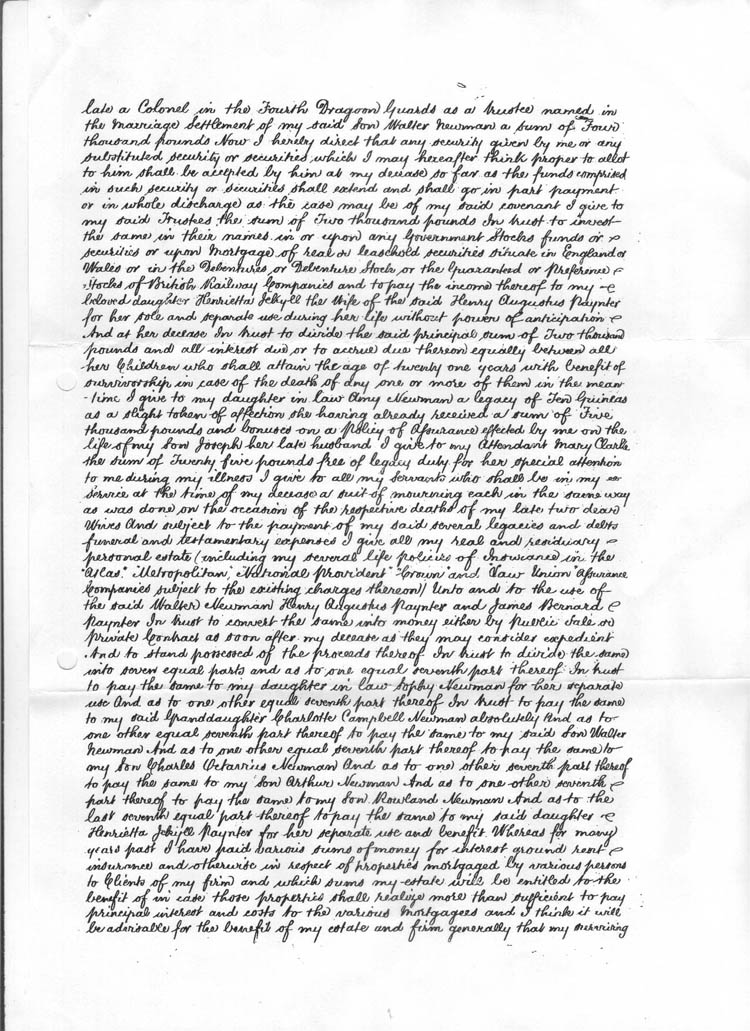

Whereas I have covenanted to pay Andrew Smythe Montague Browne late a Colonel in the Fourth Dragoon Guards as a trustee named in the marriage settlement of my said son Walter Newman a sum of four thousand pounds, now I hereby direct that any security given by me or any substituted security or securities which I may hereafter think proper to allot to him shall be accepted by him at my decease so far as the funds comprised in such security or securities shall extend or go in part payment or in whole discharge as the case may be of my said covenant.

I give to my Trustees the sum of two thousand pounds in trust to invest the same in their names in or upon any government stocks, funds or securities or upon mortgage of real or leasehold securities situate in England or Wales or in the debentures or debenture stock or the guaranteed or preference stocks of British railway companies and to pay the income thereof to my beloved daughter Henrietta Jekyll, wife of the said Henry Augustus Paynter for her whole and separate use during her life without power of anticipation, and at her decease in trust to divide the said principle of two thousand pounds and all interest accrued or due thereto between all her children who shall attain the age of twenty one years with benefit of survivorship in case of the death of any one or more of them in the meantime.

I give to my daughter-in-law Amy Newman a legacy of ten guineas as a slight token of affection, she having already received a sum of five thousand pounds and bonuses on a policy of assurance effected by me on the life of my son Joseph her late husband.

I give to my attendant Mary Clarke the sum of twenty-five pounds free of legacy duty for her special attention to me during my illness.

I give to all my servants who shall be in my service at the time of my decease a suit of mourning each in the same way as was done on the respective deaths of my late two dear wives.

And subject to the payment of my said several legacies and debts funeral and testamentary expenses, I give all my real and residuary personal estate (including my several life policies of insurance in the Atlas, Metropolitan, National Provident, Crown and Law Union assurance companies subject to the existing charges thereon) unto and to the use of the said Walter Newman, Henry Augustus Paynter and James Bernard Paynter in trust to convert the same into money either by public sale or private contract as soon after my decease as they may consider expedient, and to stand possessed of the proceeds thereof in trust to divide the same into seven equal parts and as to one equal seventh part thereof in trust to pay the same to my daughter-in-law Sophie Newman for her separate use, and as for one other equal part to pay the same to my granddaughter Charlotte Campbell Newman absolutely, and as for one other seventh equal part thereof to pay the same to my said son Walter Newman, and as to one other equal seventh part thereof to pay the same to my son Charles Octavius Newman, and as to one other seventh part thereof to pay the same to my son Arthur Newman, and as to one other seventh part thereof to pay the same to my son Rowland Newman, and as to the last seventh equal part thereof to pay the same to my daughter Henrietta Jekyll Paynter for her separate use and benefit.

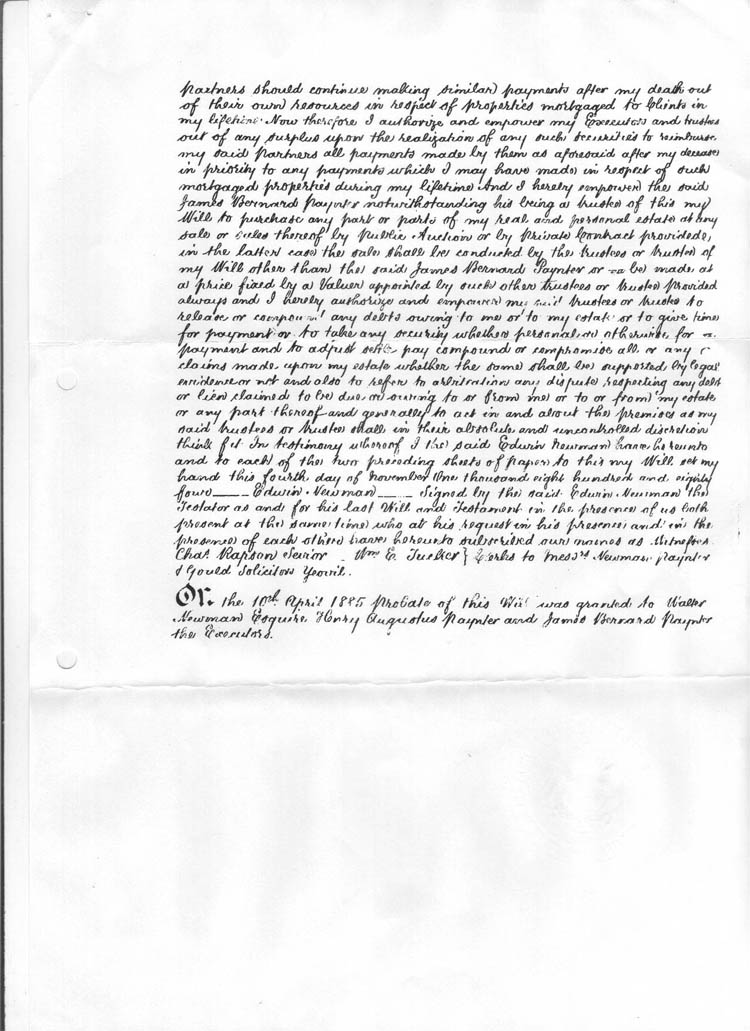

Whereas for many years past I have paid various sums of money for interest, ground rent , insurance and otherwise in respect to properties mortgaged by various persons to clients of my firm, and which sums my estate will be entitled to the benefit of in case those properties shall realize more than sufficient to pay principle, interest and costs to the various mortgagees and I think it will be advisable for the benefit of my estate and firm generally that my surviving partners should continue making similar payments after my death out of their own resources in respect of properties mortgaged to clients in my lifetime.

Now therefore I authorize and empower my executors and trustees out of any surplus upon the realization of any such securities to reimburse my said partners all payments made by them as aforesaid after my decease in priority to any payments which I may have made in respect of such mortgaged properties during my lifetime. And I hereby empower the said James Bernard Paynter notwithstanding his being a trustee of this my will, to purchase any part or parts of my real or personal estate at any sale or sales thereof at public auction or by private contract provided in the latter case that the sale shall be conducted by the trustees or trustee of my will other than James Bernard Paynter or be made at a price fixed by a valuer appointed by such other trustees or trustee to release or compound any debts owing to me or my estate or to give time for payment or to take any security whether personal or otherwise for payment and to adjust, settle, pay compound or compromise all or any claims made upon my estate whether the same shall be supported by legal evidence or not and also to refer to arbitration any disputes respecting any debt or lien claimed to be due or owing to or from me or to or from my estate or any part thereof and generally to act in and about the premises as my said trustees or trustee shall in their absolute and uncontrolled discretion think fit.

In testimony whereof I the said Edwin Newman have hereunto and to each of the two preceding sheets of paper to this my will set my hand this fourth day of November one thousand eight hundred and eighty four – Edwin Newman etc etc.

.....................................................

On 10th April 1885 probate of this will was granted to Walter Newman Esquire, Henry Augustus Paynter and James Bernard Paynter, the executors.

|

|

|||

| Estate Value | . |

£31,189 |

|

| Charlotte Campbell Newman | Legacy | £1,000 |

|

| Andrew Smythe Montague Browne | Covenant | £4,000 |

|

| Henrietta Jekyll Paynter | Trust | £2,000 |

|

| Amy Newman [widow of Joseph Jekyll Newman] | Legacy | £10 |

|

| Mary Clarke | Gift | £25 |

|

| Unspecified debts, funeral and other expenses | say | £2,151 |

|

| Balance | £21,003 |

||

| Sophie Newman | Inheritance (one 7th equal part) | £3,000 |

|

| Charlotte Campbell Newman | Inheritance (one 7th equal part) | £3,000 |

|

| Walter Newman | Inheritance (one 7th equal part) | £3,000 |

|

| Charles Octavius Newman | Inheritance (one 7th equal part) | £3,000 |

|

| Arthur Newman | Inheritance (one 7th equal part) | £3,000 |

|

| Rowland Newman | Inheritance (one 7th equal part) | £3,000 |

|

| Henrietta Jekyll Paynter | Inheritance (one 7th equal part) | £3,000 |

|

Legacy Duty

copied from http://en.wikipedia.org/wiki/Inheritance

Tax (United_Kingdom)

From 1796, small inheritance taxes, then called legacy, succession and estate duties were collected, in England and Wales on estates over a certain value by stamping deeds and by stamping wills admitted to probate, similarly to stamp duty. The value varied and the scope of estate duty became gradually extended as the socio-economic parish level land taxation system obsolesced as a result of the Industrial Revolution. From 1857, estates worth over £20 were taxable but duty was rarely collected on estates valued under £1,500. Death duties were introduced in 1894 and the rates have been increased which led in many cases for the first time to the breaking up of large estates. Estate Duty began, at a more typical rate of tax, starting in 1914 under the First Asquith ministry that was a breakthrough in constitutional terms and social terms by introducing the People's Budget and the first written right of the House of Commons to ascendancy in the Parliament of the United Kingdom under the Parliament Act 1911.

The following also appears under the heading "Succession Duty":

Succession duty, in the English fiscal system, "a tax placed on the gratuitous acquisition of property which passes on the death of any person, by means of a transfer from one person (called the predecessor) to another person (called the successor)." In order properly to understand the present state of the English law it is necessary to describe shortly the state of affairs prior to the Finance Act 1894—an act which effected a considerable change in the duties payable and in the mode of assessment of those duties.

The principal act which first imposed a succession duty in England was the Succession Duty Act 1853. By that act a duty varying from 1% to 10% according to the degree of consanguinity between the predecessor and successor was imposed upon every succession which was defined as "every past or future disposition of property by reason whereof any person has or shall become beneficially entitled to any property, or the income thereof, upon the death of any person dying after the time appointed for the commencement of this act, either immediately or after any interval, either certainly or contingently, and either originally or by way of substitutive limitation and every devolution by law of any beneficial interest in property, or the income thereof, upon the death of any person dying after the time appointed for the commencement of this act to any other person in possession or expectancy." The property which is liable to pay the duty is in realty or leasehold estate in the United Kingdom and personalty - not subject to legacy duty - which the beneficiary claims by virtue of English, Scottish or Irish law. Personalty in England bequeathed by a person domiciled abroad is not subject to succession duty. Successions of a husband or a wife, successions where the principal value is under £100, and individual successions under £20, are exempt from duty. Leasehold property and personalty directed to be converted into real estate are liable to succession, not to legacy duty.

Note: http://www.nationalarchives.gov.uk/records/research-guides/death-duty-records-1796-to-1903.htm states that "The term 'death duties' covers three taxes: Legacy Duty, Succession Duty and Estate Duty however it does not define them or the differences between them.

Page updated 23 Dec 2014: Transcription of will added plus notes on Legacy Duty